{kind=link}

Identifying the core problem

Many Mexican households juggle irregular income, sudden expenses, and limited savings. Drivers, gig workers, and micro-entrepreneurs face fluctuating demand that breaks traditional cash flow models. Practical solutions must treat household finances like a microgrid: balance inflows against variable loads, prioritize critical circuits, and add short-term buffering. Platforms such as didi prestamos are increasingly positioned to provide that buffer with targeted short-term credit and faster access to capital.

Why traditional tools fail families

Bank loans and long-term credit products rely on steady pay cycles and formal underwriting. For many households that lack formal payroll records, those products are slow, rigid, and misaligned with real cash cycles. Liquidity gaps appear suddenly — medical bills, school fees, or a car repair can push a family into payment delinquency within days. The mismatch between financial product cadence and household cash flow is the root technical failure to address.

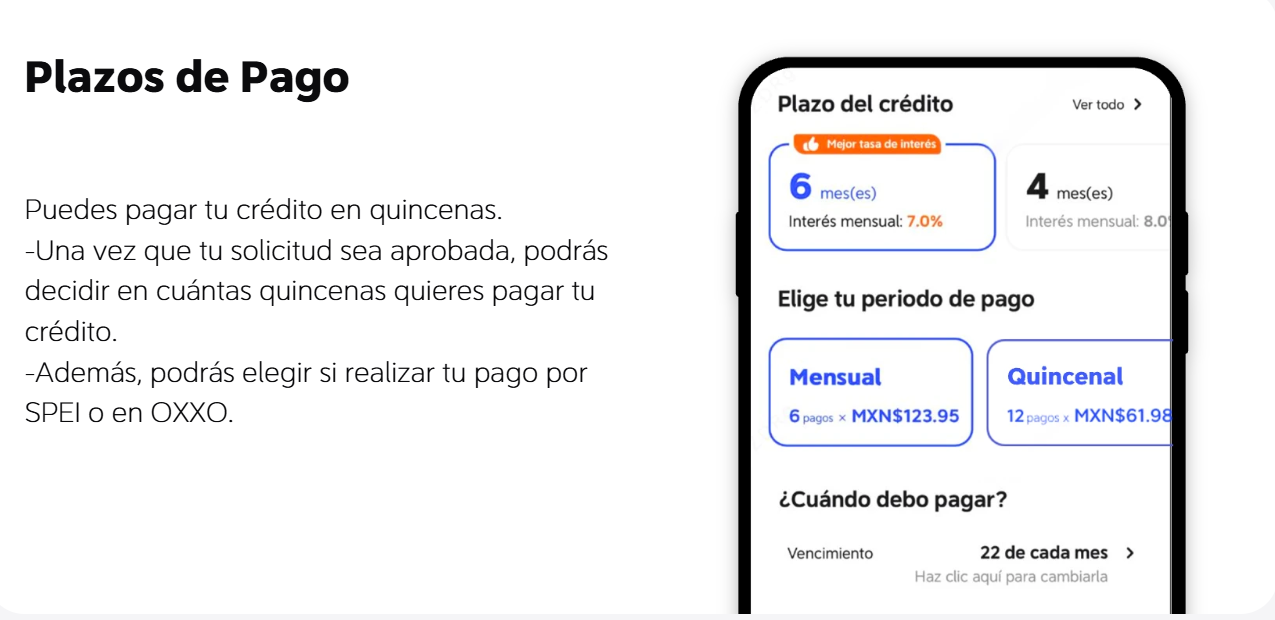

How DiDi Finanzas fits into the solution

Viewed through an engineering lens, DiDi Finanzas acts like a distributed storage system for capital: it offers short-term, accessible loans calibrated to gig income patterns. By integrating earnings data and faster underwriting models, such systems reduce time-to-fund and lower friction for users. That operational focus supports practical cash flow forecasting for households, enabling smoother consumption smoothing and fewer emergency measures.

Real-world anchor: recent demand shocks and their lessons

The COVID-19 pandemic exposed fragility in informal income streams across Mexico City and other urban centers. Drivers and delivery workers saw demand drop sharply in early 2020, then rebound unevenly—leaving many with unpredictable monthly receipts. That event underscored the need for flexible financial products that respond quickly to changes in income. Providers that optimized approval velocity and offered transparent APRs helped users avoid long-term debt traps.

Common implementation mistakes to avoid

Designing household cash solutions requires avoiding predictable errors:

– Overextending loan tenure for short-term needs; extended terms increase total interest paid. – Ignoring transparent pricing: APR clarity matters for trust and repeat use. – Neglecting integration with earnings data for better underwriting and repayment alignment.

These mistakes create perverse incentives and harm long-term financial health—so engineers and product teams should treat user cash flow as a system constraint, not a variable to be masked.

Practical steps families can use now

Families and gig workers can apply straightforward tactics to stabilize cash flow: maintain a small liquid buffer equivalent to two weeks of essential costs; map predictable inflows versus outflows weekly; use short-term credit only for bridging predictable gaps and not recurring deficits. When short-term credit is required, prefer options that disclose fees and permit flexible repayment aligned with earnings — examples include services described as prestamos en linea al instante that promise fast funding without opaque penalties.

Measuring success — metrics that matter

Evaluate any financial tool by three operational metrics: approval time (hours vs. days), effective cost (true APR including fees), and repayment alignment (does repayment schedule sync with income cadence). Monitoring these metrics keeps solutions practical and avoids debt accumulation. Deploy simple dashboards or a monthly ledger to track them—small data goes a long way.

Advisory: golden rules for selecting household cash-flow tools

1) Prioritize speed and transparency — faster funding with clear APRs reduces emergency risk. 2) Match term to need — use short-term credit for temporary gaps, avoid using it for recurring deficits. 3) Check integration with income sources — platforms that reference ride-share or delivery earnings enable smarter underwriting and fairer repayment plans.

These rules form the evaluation backbone for anyone choosing tools that support steady household liquidity.

Final reflection

Optimizing family cash flow requires practical engineering: simple buffers, aligned repayment, and transparent pricing. Institutions that design products with those constraints succeed in real contexts—helping people maintain day-to-day stability and avoid long-term strain. DiDi Finanzas fits into that framework as a pragmatic solution integrated with gig-era earnings — a steadying element for household budgets. —